Archive for the ‘News’ Category

As a follow-up to their ground-breaking white paper, Bassford Remele Attorneys Patrick Newman, Jessica Klander, and Tal Bakke joined ARA on June 13 to answer pressing questions about data privacy. During the hour-long webinar, the professionals at Bassford Remele covered a wide range of topics, including:

- How to identify and respond to breaches;

- If/when you must provide notice of a breach;

- Who is responsible for deleting consumer information from vehicles;

- …and more!

Miss the webinar? Listen in at the link below to learn how you can protect your business from costly data breaches and privacy issues.

Listen Here

Proceed With Caution: Data Collection and Connected Cars

Data privacy is a growing and serious issue that can lead to severe monetary penalties, averaging $3.86 million per data breach in 2020.

In fact, some states have already passed laws that may impact the recovery industry, including California, New York, and Virginia.

In ARA’s latest groundbreaking white paper — authored by Attorneys Patrick Newman, Tal Bakke and Marie Brekke of Bassford Remele — you’ll learn how to stay ahead of the data privacy curve and which compliances your business should be considering now.

Read the full white paper

HERE.

Strategic Partnership Will Provide Crucial Educational Materials for Repossession Industry

IRVING, Texas—The American Recovery Association (ARA) and Bassford Remele have announced a groundbreaking partnership that will bring unparalleled educational and compliance perspectives to lending and repossession communities alike.

The ARA is excited to utilize Bassford Remele’s trusted compliance and litigation experience to assist ARA members in developing a “Culture of Compliance” that will stand out across the recovery industry. The partnership will kick-off with an industry-wide webinar on Wednesday, April 7.[1]

Bassford Remele is a full-service litigation firm based in Minneapolis, Minnesota. Bassford has built strong relationships with business leaders in a number of industries, including credit and collections, background screening, secured lending and leasing, construction, agribusiness, health care, and technology. Its lawyers have a depth of experience in various practice areas, including defense of consumer law claims (FDCPA, FCRA, TCPA, wrongful repossession), collection and replevin proceedings (UCC Articles 2A and 9), creditor representation in bankruptcy, data privacy compliance and litigation, as well as many others.

Bassford regularly litigates cases through trial in the district courts, handles appeals at the state and federal level, and represents clients in regulatory investigations and proceedings. Bassford’s lawyers are licensed to practice in numerous state and federal jurisdictions across the country.

“We are honored to have a company with the reputation of Bassford Remele partner with our association with the intent of taking our CCRS program to the next level and supporting our mission to equip recovery professionals with the knowledge needed to succeed in today’s ever-changing landscape,” said ARA President Dave Kennedy. “This is another great step in our efforts to unite the industry and provide our members with tangible resources that can benefit their businesses long-term.”

As part of this new partnership, ARA will be able to provide additional compliance materials to help navigate legislative perspectives. ARA is also excited to announce Bassford Remele’s participation in ARA’s new online community, Repo.Tradewing.com.

“We are very excited to work with the ARA and its membership on the compliance and litigation fronts,” said Bassford Remele Shareholder Patrick Newman. “More than anything we look forward to being a resource for the recovery and remarketing industry.”

For more information about ARA, its partnerships, and its member benefits, please visit repo.org. For more information on Bassford Remele, visit bassford.com.

###

About American Recovery Association, Inc.

American Recovery Association (ARA) is the world’s largest association of recovery and remarketing professionals. ARA members specialize in locating and repossessing collateral on behalf of lending institutions, including banks, savings institutions, finance companies, credit unions, rental/leasing companies, and auto, truck, and equipment dealers. ARA is a nonprofit association whose members serve 27,000 national and international cities. All members are certified independent business operators. For more information, call 972.755.4755 or visit the website at www.repo.org.

About Bassford Remele

Bassford Remele, P.A. is a full-service litigation firm located in Minneapolis, Minnesota. With unparalleled courtroom and trial experience, Bassford Remele devotes its practice to providing trial and appellate representation, as well as dispute resolution, for regional, national, and international clients in a variety of complex business and commercial litigation. Founded in 1882, Bassford Remele is recognized as a leading Minnesota firm by Chambers USA: America’s Leading Lawyers for Business in 2020. The firm is ranked nationally and regionally in the 2021 U.S. News – Best Lawyers® “Best Law Firms” list in 19 practice areas, including Bet-the-Company Litigation and Commercial Litigation. It is also among Forbes’ “America’s Top Trusted Corporate Law Firms.” For more information, visit their website at https://www.bassford.com

[1] The educational materials referenced herein are not intended to be, nor are they, legal advice. Nothing stated herein, or in any of the referenced educational materials, creates an attorney-client relationship between ARA membership and Bassford Remele PA. No such relationship will be created absent an executed retention agreement with Bassford Remele PA.

Dear Repossession Industry,

On Sunday night, President Trump signed into law the Consolidated Appropriations Act which combined the FY2021 federal spending bill with the Phase 4 COVID‐19 relief package. Our months‐long effort to convince lawmakers to oppose the inclusion of any restriction on repossessions, including a long‐term moratorium, were successful. In addition to excluding the repossession moratorium, the final bill included a number of changes to small business aid programs which struggling repossession companies should consider as a source of financial support. Please note, this week, Congress will take several steps to amend the Phase 4 bill, however, as currently discussed, none of this week’s legislative activity would impact the small business programs described in this memo. This memo summarizes the key elements of those small business aid programs that may apply to collateral recovery companies.

Paycheck Protection Program: Second Round of Loans

- $284.5 billion for a “second draw” program of PPP.

- Defines eligibility for the PPP second draw as small businesses that have no more than 300 employees and demonstrate at least a 25 percent reduction in gross revenues between comparable quarters in 2019 and 2020.

- Establishes a maximum loan size of 2.5 times the average monthly payroll costs, up to $2 million.

- Borrowers receive full loan forgiveness if they spend at least 60% of their PPP second draw loan on payroll costs over a time period of their choosing between 8 weeks and 24 weeks.

- Includes set‐asides to support first‐time PPP borrowers with 10 or fewer employees, second‐time PPP borrowers with 10 or fewer employees, first‐time PPP borrowers who have been made newly eligible, and second‐time returning PPP borrowers. Additionally, provides for a set‐aside for loans made by community lenders.

Paycheck Protection Program: General Improvements

- Expands PPP allowable and forgivable expenses to include supplier costs on existing contracts and purchase orders, including the cost for perishable goods at any time, costs relating to worker protective equipment and adaptive costs, and technology operations expenditures.

- Provides needed assurances to PPP lenders that no enforcement action could be taken against a lender who originated the loan in good faith, complied with all regulations, and relied in good faith on a borrower’s certification and documentation.

- Enhances borrower flexibility by allowing borrowers to select their loan forgiveness covered period between 8 weeks and 24 weeks.

- Simplifies the forgiveness application process for smaller loans up to $150,000 while increasing SBA’s ability to audit and review forgiven loans.

- Allows PPP borrowers to include additional group insurance payments when calculating their PPP payroll costs. This would cover insurance plans such as vision, dental, disability and life insurance.

- Allows borrowers who returned all or part of their PPP loan to reapply for the maximum amount applicable. It also allows lenders to recalculate borrower’s loan amounts due to changes in regulations regardless of whether SBA Form 1502 has been submitted.

- Establishes a procedure in the bankruptcy process if the Administrator determines certain small business debtors in Chapter 11 are eligible for PPP loans.

- Eliminates the requirement that EIDL advances be subtracted from PPP forgiveness

Enhancements to SBA’s Lending Programs:

- $3.5 billion for 7(a) program.

- Temporarily enhances the terms of the 7(a) loan program by increasing the loan guarantee to 90 percent and offering reduced or no fees for the borrower and the lender. Additionally, it would temporarily increase the 7(a) express loan limit and loan guarantee to provide access to needed working capital.

- Temporarily eliminates fees for the 504 loan program and favorable terms for refinancing loans.

- Increases the aggregate loan limit for microloan intermediaries in order to ensure intermediaries have increased capacity to make loans to underserved and underbanked borrowers.

- Extends the Small Business Debt Relief program, Section 1112 of the CARES Act, which would defer payments of principal and interest on new and existing SBA 7(a), 504, and Microloan programs for eligible entities.

Increased Transparency and Accountability in SBA Programs:

- Mitigates fraud by requiring new measures for the SBA to verify eligibility for EIDL Advance grants.

- Increases transparency of SBA’s PPP forgiveness audit and review process by requiring the SBA to submit a detailed forgiveness audit plan to Congress within 30 days of enactment. Appropriates $50 million to support SBA’s PPP audit authority.

- Prohibits PPP loan proceeds to be used for lobbying activities.

- Requires the President, Vice President, the head of an Executive department, or a Member of Congress as well as their spouse to disclose this status when receiving forgiveness on a Paycheck Protection Program initial loan. Prohibits these individuals from obtaining a future PPP loan.

COVID Stimulus Package Includes Deductibility of PPP Loans

Section 276 of the package clarifies that gross income does not include any amount that would otherwise arise from the forgiveness of a Paycheck Protection Program (PPP) loan. This provision also clarifies that deductions are allowed for otherwise deductible expenses paid with the proceeds of a PPP loan that is forgiven, and that the tax basis and other attributes of the borrower’s assets will not be reduced as a result of the loan forgiveness. The provision is effective as of the date of enactment of the CARES Act. The provision provides similar treatment for Second Draw PPP loans, effective for tax years ending after the date of enactment of the provision

Cordially,

J. Patrick Altes

Dear Repossession Industry,

Good news! We have heard that the Phase 4 bill being put forward today by Congress does NOT contain any language regarding a repossession moratorium.

We have heard from some sources that this whole endeavor of hiring lobbyists has been a waste of time and money. Nothing is further from the truth, and only exposes the critics’ ignorance of the machinations of the US Congress. There was a 180+ day moratorium (would have been longer) in the HEROES Act that was presented to the Senate, to which this Phase 4 is a response. To sit idle on the sidelines, while our industry’s future was in the gunsights of the House, would have been foolish.

However, keep your eye on the ball…..we actually believe the real problems will come once the new administration takes office; they have publicly and repeatedly committed to reviving the CFPB and ramp up their enforcement actions. They have specifically mentioned the auto lending and collection processes. We have every reason to expect that more draconian repossession-relations directives will be considered, and to have a voice at the table of THOSE discussions is key as well.

The Repo Alliance and their lobbyists represent a tremendous effort to protect the future of the repossession industry as it comes under review by the US government. It certainly needs your support, and for the few in our industry that question its efficacy, at least show enough wisdom to hold your complaints until this fight is over. Never has our industry been at such risk through legislation or policy-making on a national level.

We have seen similar legislation and moratoriums in many states. California in particular was extremely aggressive in trying to pass moratoriums and eliminate self-help repossession until 2022. Many states follow legislation that is passed in California. It’s critical for the repossession industry to maintain a presence not only during the pandemic but for years to come.

Cordially,

J. Patrick Altes

ARA Industry Whitepaper: Specialty Equipment

At ARA, we share your goals and are striving for cost-effective, safe recovery of collateral. When recovering collateral, if you are relying on out of date equipment, it might be time to change. The current fee structure and approval systems in place in our industry today are limiting the recovery professional’s options for utilizing the proper equipment to recover automobiles equipped with modern technology.

ARA has put together this Specialty Equipment Whitepaper to help recovery professionals in our industry educate lenders on the real-world challenges their recovery professionals face.

ARA is YOUR resource for critical industry issues and standards. Click the video below to watch our latest educational industry video surrounding specialty equipment.

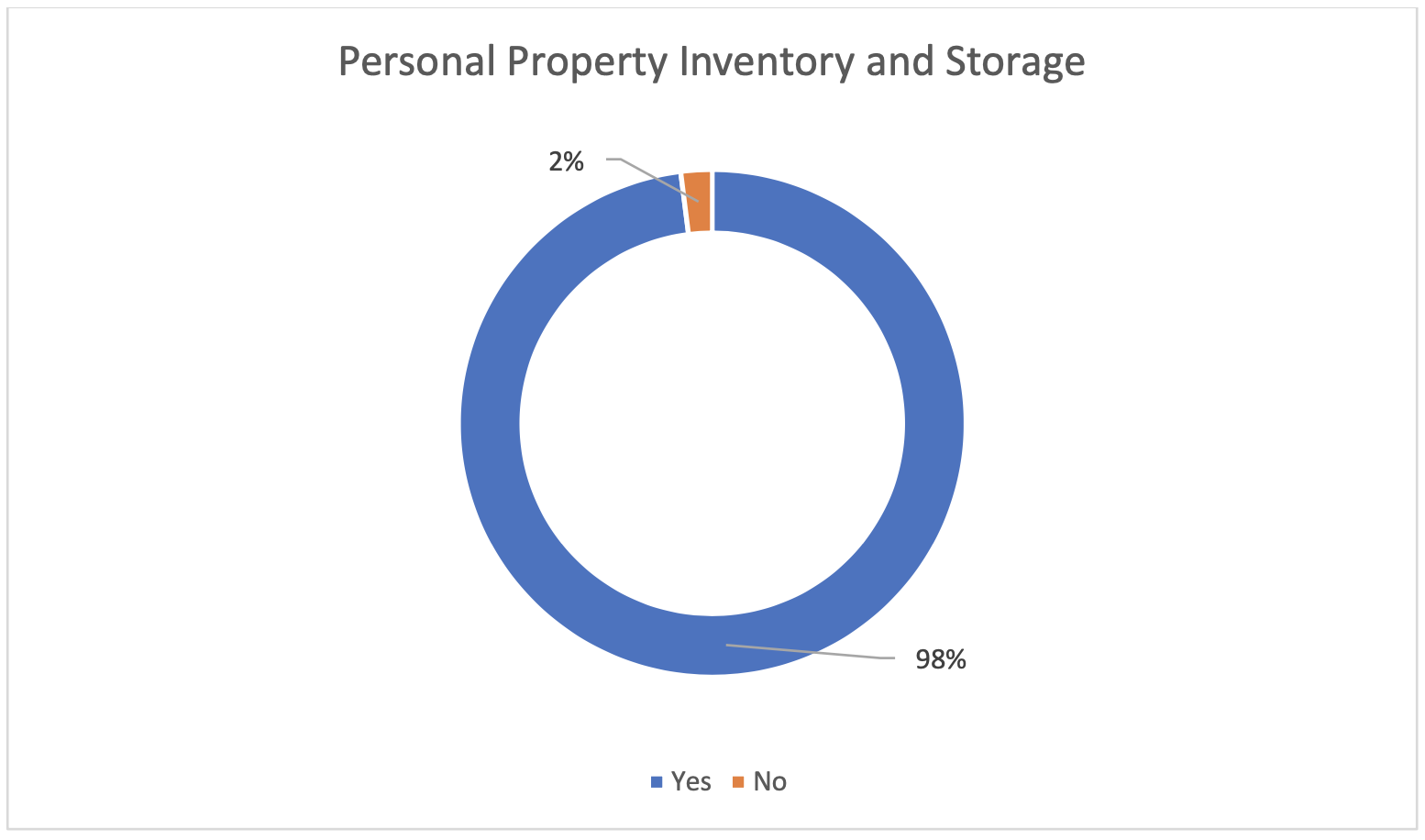

What Personal Property Fees Should

You Be Charging?

For many years now, we have been bankrupting ourselves thanks to the inability of repossession agents, lenders and forwarders to come together and address issues head-on. With our new whitepaper series, “Repossession Matters,” ARA will be addressing these issues and presenting revenue models to allow for repossession agencies to operate in a viable and sustainable manner.

The goal of the Repossession Matters Series will be to raise understanding among us and lead with one clear voice as an industry – something that up until this point has not been achieved.

With our first Whitepaper Video presentation, ARA has taken a deep dive into the true cost and potential risk surrounding Personal Property Fees.

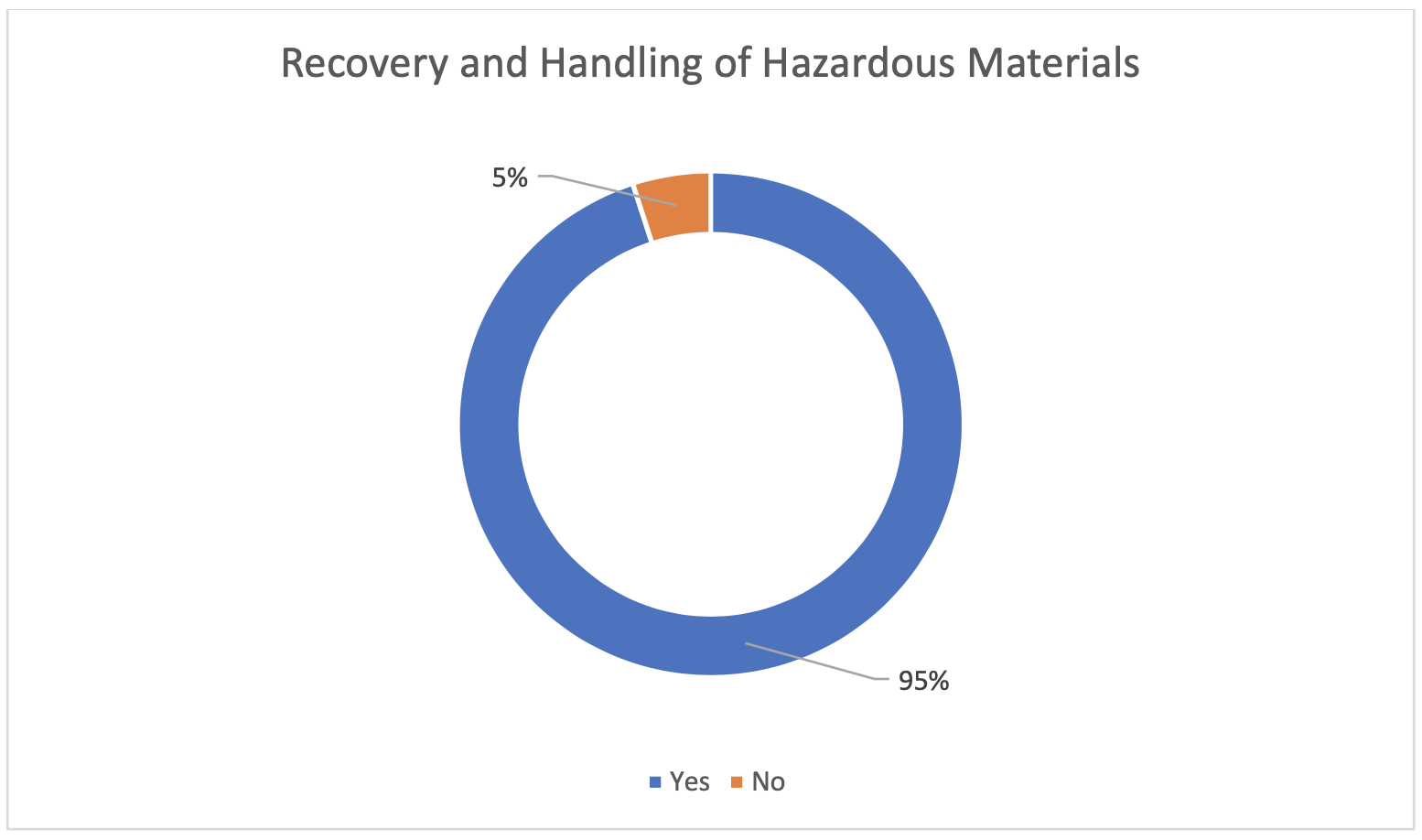

Every day, members of our industry put themselves at risk handling potentially hazardous materials from recovered vehicles, and dealing with personal property from repossessed vehicles is one of the most difficult aspects of the recovery professional service, making it even more important to charge the correct fees for handling belongings.

So, what fees should you be charging for the care and storage of personal property? Click below to watch our first of many industry wide Repossession Matters video!

Q&A Webinar with Industry Lobbyist Jennifer LaTourette

On July 22nd, ARA hosted a question and answer webinar with our industry Lobbyist from Van Scoyoc Associates, Jennifer LaTourette!

As many of you know, pending legislations throughout Washington have threatened the viability of small businesses and our industry as a whole.

In response to the various legislations, ARA, with the support of the Repo Alliance, has retained the service of Jennifer LaTourette, an experienced lobbyist who can advocate for our interests in Washington through this crisis and beyond.

Jennifer joined ARA to discuss how she is advocating for the industry in Washington D.C. against these detrimental legislations and why having a lobbyist is important in situations like ours.

You don’t want to miss this insightful webinar – click below to watch!

The Cost of COVID-19 on the Industry

Over the last few weeks, ARA has been assessing, researching and creating content which will put forth a clear and present argument for radical change within the pricing structures of our industry, which will be beneficial to all parties. However, the spectrum of issues is a broad one and cannot be tackled with levity. These services are essential to the entirety of the auto finance business and must be valued as such – by all parties involved.

As part one of our multi-part series, ARA has put together a stance on COVID-19 measures – click below to view. Contained within are suggestions for repossessors, lenders and forwarders alike because again, we must work together to effect the sweeping change so desperately needed. Click below to see the what we put together.