CCRS Certification

Understand Why This Certification is Important to You

We know you have choices when you want to verify the credentials of a repossession professional.

The Certified Collateral Recovery Specialist (CCRS) certificate provides comfort and reassurance you’ve made the right choice in selecting your repossession agent. It shows your repossession professional has passed all current repossession testing standards and will take care of your concerns with the highest possible professionalism.

Note: If you’re a repossession agent looking to access the ARA Compliance System, see our Navigation Guide into the Compliance System. If you’re a lending professional looking to use the CCRS, contact us at (972) 755-4755.

The CCRS Difference

So, what really makes CCRS different from other certifications in the repossession industry?

It begins with our ever-evolving and highly-detailed educational materials. In the current repossession environment, it’s crucial we keep up to date on today’s compliance standards and how repossessions are performed. This is the confidence you should demand and expect when you see a repossession professional display a Certified Collateral Recovery Specialist certificate in the office.

And while we contend with the complex repossession issues of the present day, our training and testing also blend the past with the present to provide historic guidance into the future of the repossession industry.

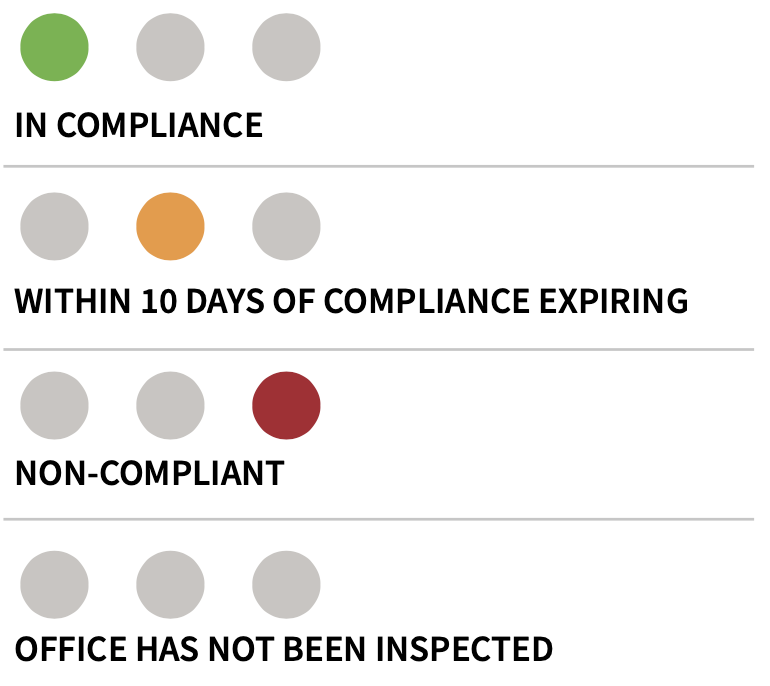

Compliance Monitoring System

Easily monitor compliance for each of our members using our Find A Recovery Specialist Directory. Enter the zip code or city and state into the search box and you will receive results for every ARA member who works in the requested area.

Beside each memberʼs name, you will see three lights. If the light is green, the member is currently in compliance with ARA compliance standards. If the light is yellow, the member is within 10 days of a document expiring. Lastly, if the light is red, the member has not yet met ARAʼs compliance standards. If there are three grey lights, the member has not yet been inspected – they may have met the standards but that has not been independently verified.

Exploring the CCRS Subject Matter

Inside the company or individual test portal, it’s important to review the study materials available, as each test is crafted to ensure your knowledge of the required material for your CCRS certification.

Select a tab below for more information.

Fair Debt and Collection Practice ACT

The FDCPA is a federal law that limits the behavior and actions of third-party debt collectors who attempt to collect debts on behalf of another person or entity.

Gramm-Leach-Bliley Act

The GLBA addresses concerns relating to consumer information privacy when a financial institution shares a consumer’s non-public information or personally identifiable information (NPI/PII) with unaffiliated third parties.

Unfair, Deceptive, or Abusive Acts or Practices

In the Unfair, Deceptive, Abusive Acts or Practices Act, the FTC defines a deceptive act or practice as a material representation or omission that misleads or is likely to mislead consumers acting reasonably under the circumstances.

Servicemembers Civil Relief Act

It is imperative that all employees working for recovery companies in any capacity understand the importance of the rights afforded to individuals protected by the SCRA from repossession of their vehicle.

Telephone Consumer Protection Act

The primary purpose of the TCPA is to regulate the number of nuisance calls and messages, including automated dialing technology and pre-recorded messages, and to safeguard consumer privacy by restricting companies (including individual repossessing firms and individuals) from engaging in unwanted telemarketing communication practices by telephonic and text-based telemarketing.

Americans with Disabilities Act (ADA)

The ADA is one of America’s most comprehensive pieces of civil rights legislation. It prohibits discrimination and guarantees that people with disabilities have the same opportunities as everyone else to participate in the mainstream of American life.

Bankruptcy

This study guide contains key information and insights from the government agencies that develop and/or enforce the provisions of the US Bankruptcy Reform Act.

Field Agent Daily Startup Routines

As described in the title, this section will help you learn how to best prepare for a day in the field: preparing your truck, obtaining important information about your scheduled assignments, and planning your strategies for the day.

Field Agent Safe Driving

As a repossessions agent, it’s important that you are safer behind the wheel than other drivers on the road. You will learn key defensive driving tactics that will help you improve your ability to avoid collisions, including how to maintain conscious and consistent development of knowledge, alertness, and foresight in recognizing potential crash situations as they appear. It is critical to exercise good judgment and improve your skills so you can better protect yourself and others.

Workplace Violence

Workplace experts recommend that all employees are trained in nonviolent response and conflict resolution to reduce the risk that volatile situations will escalate to physical violence. A critical aspect of this training addresses hazards associated with specific tasks or worksites, complete with relevant prevention strategies.

Complaint Handling

The Consumer Finance Protection Bureau mandates that financial institutions and their third-party vendors have written CONSUMER COMPLAINT policies and procedures. This section covers those nuances.

Color of Law

The “COLOR OF LAW” is a legal doctrine that provides protection to a citizen from the actions of both government officials and private citizens whose action arises from a power or authority granted by a state law. We take a detailed look at this section with great care.

Social Media

We live in an era when an employer’s basic code of conduct can be overwhelmed by a swell of enticements to surf the Web and post words, pictures, and information that are best kept offline. It has become increasingly important that companies establish and make unequivocally clear their rules on social media in the workplace. This section takes a hard look at today’s issues when it comes to this relatively new form of indirect and direct communication.

We look at compliance from a holistic view.

Every owner who is an ARA Member goes through a series of interviews, financial vetting, and background checks to be a member. But it’s the branches of his or her company tree we take a deeper look into. This is where the CCRS program ensures that gold standard of confidence when you send out a voluntary or repossession assignment. Training and testing aren’t simply lip service with the ARA – they’re a way of life.

If you have questions or would like to learn more, please contact Home Office at homeoffice@americanrecoveryassn.org. If you’re a repossession agent looking to access the ARA Compliance System, see our Navigation Guide into the Compliance System. If you’re a lending professional looking to use the CCRS, contact us at (972) 755-4755.

ARA has sole authority to issue a certificate based only on information supplied by the participant and their achievement (i.e., application, education/training, assessment(s)).

a) The purpose and scope of the program are to train collateral recovery owners and their employees to understand and execute properly the Federal/State Consumer Protection Laws as set forth by State and Federal Regulators.

b) Participant or Participant’s employee must be a member of good standing with the American Recovery Association.

c) Student is provided with study materials. There is a pretest to access their beginning level of knowledge. Participant must pass a test at the end of each training module with a minimum of an 80% passing score.

The American Recovery Association does not discriminate against any individual that may be covered under the American with Disabilities Act. The CCRS test is an online test that the participant takes at a computer and location of their choosing. All participants have the same pre-course requirements and take the exact same tests. The test can be taken at any computer, so it poses no problem to accommodate any student who meets the definition and qualifications of the Americans with Disabilities Act.

The American Recovery Association is the sole owner of all educational and testing materials and is the one and only issuing entity for completion certificates for students who have successfully completed all modules.